“The office was real. The events were real. The people promoting it were real. The question regulators eventually asked was whether the investment opportunity itself was real.”

For months, anyone questioning BG Wealth Sharing was told they simply did not understand the opportunity.

Critics were accused of spreading fear. Victims were told they were being negative. Promoters insisted the trading was real, the returns were real, and that a man known as Professor Stephen Beard was guiding thousands of people toward financial freedom through a revolutionary cryptocurrency trading platform.

I heard those claims repeatedly throughout my investigation.

I watched the presentations. I reviewed the marketing material. I listened to the recruitment calls. I spoke directly with promoters and members who passionately defended the opportunity. Like so many schemes before it, BG Wealth Sharing was sold as something far bigger than an investment platform. It was presented as a movement. A community. A chance for ordinary people to change their lives.

While many of the individuals behind the operation remained hidden behind websites, apps and anonymous leadership structures, some promoters stepped into the spotlight. Few embraced that role more publicly than Richard Chea and Sumana Chea.

The Utah-based couple became some of the most visible faces associated with BG Wealth Sharing in the United States. They appeared at events, helped promote the opportunity, welcomed people into a dedicated BG Wealth Investor Centre, and became central figures in the company’s expansion efforts throughout Utah. To supporters, they represented success. To prospective investors, they helped create an appearance of legitimacy. If there were doubts about the company, the existence of physical offices, public events and local leadership gave many people confidence to ignore them.

That confidence would eventually collide with reality.

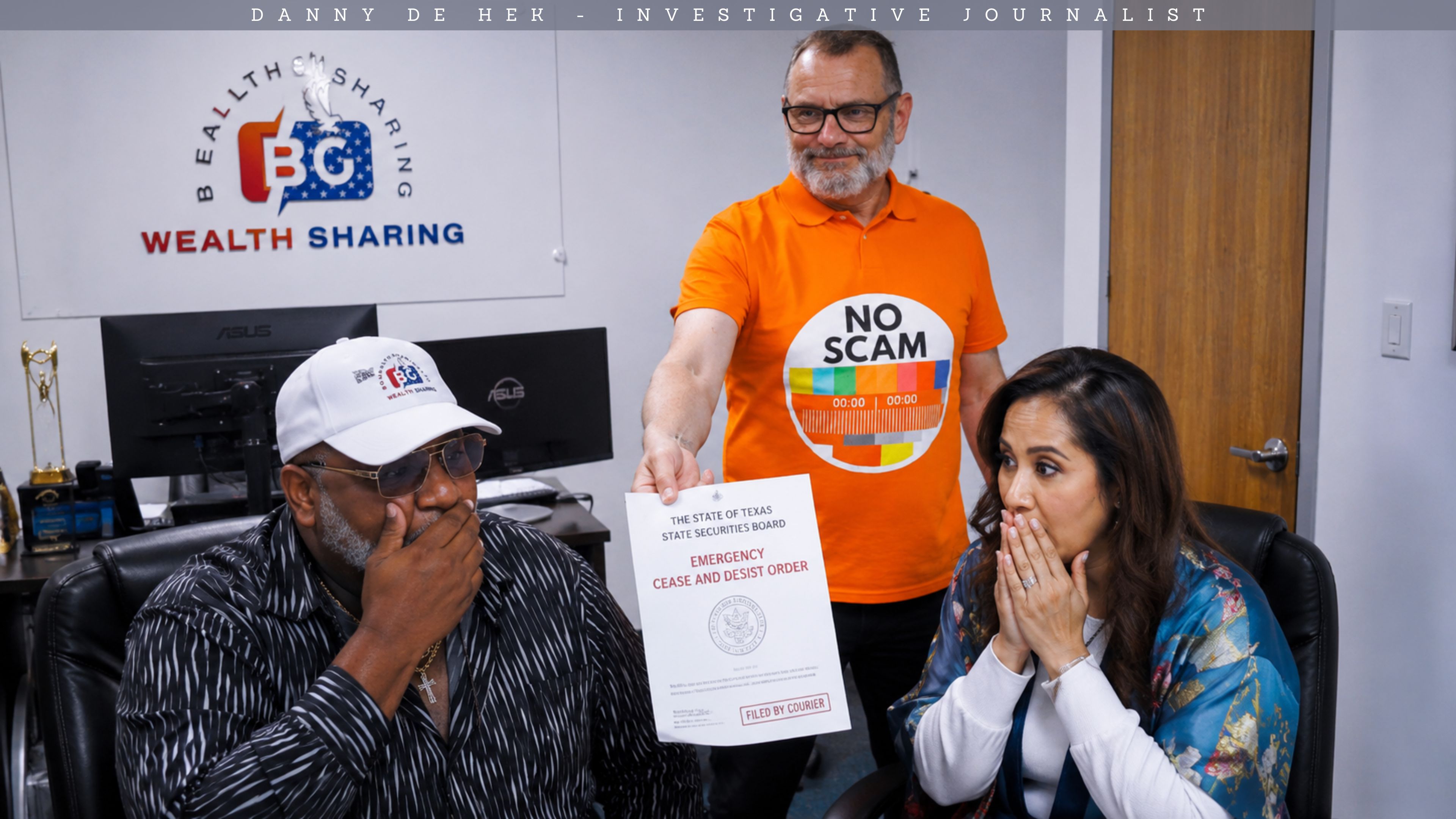

On June 1, 2026, the Utah Division of Securities issued an Emergency Order to Cease and Desist naming not only BG Wealth Sharing, DSJ Exchange and HQI Exchange, but also Richard Chea and Sumana Chea themselves. The order alleges that respondents were involved in an international cryptocurrency MLM Ponzi and advance-fee fraud scheme that targeted investors while making fraudulent guarantees, using fabricated regulatory affiliations and continuing recruitment efforts despite mounting regulatory concerns.

This is an important distinction.

For months, much of the discussion surrounding BG Wealth Sharing focused on anonymous operators, mysterious trading systems and the fictional character known as Professor Stephen Beard. The Utah action shifts part of that focus back to the people who were standing in front of audiences, hosting events, recruiting members and encouraging others to trust the opportunity.

This article examines the allegations outlined by Utah regulators, the role Richard and Sumana Chea allegedly played in promoting BG Wealth Sharing, the warning signs that emerged along the way, and how two of the scheme’s most visible promoters ultimately found themselves named in a government enforcement action.

Because when an investment opportunity collapses, the most important questions are often not about the website.

They are about the people who persuaded others to trust it.

I think this introduction is much stronger because the government warning remains the centrepiece of the story, while still pulling readers into the investigation and setting up the next section: The Public Faces Of BG Wealth Sharing In Utah.

The Public Faces Of BG Wealth Sharing In Utah

One of the biggest mistakes investors make when evaluating opportunities like BG Wealth Sharing is focusing exclusively on the company while ignoring the people promoting it.

Websites can be registered anonymously. Domains can be replaced overnight. Trading platforms can disappear without warning. But recruitment happens through people. Investors are far more likely to trust a recommendation from a friend, family member or respected community figure than they are to trust an unknown website on the internet. That is why promoters play such a critical role in the growth of these schemes. They become the bridge between the opportunity and the public.

According to the Utah Division of Securities, Richard Chea and Sumana Chea were not passive participants. The Emergency Order identifies them as local agents, managers and MLM recruiters for BG Wealth Utah. Regulators describe Richard as a longtime MLM enthusiast who promoted multiple investment opportunities and identify him as the registered agent and manager of BG Wealth Sharing Ltd. Liability Company in Utah. The order further notes that neither Richard nor Sumana held securities licences or registrations with Utah regulators, the SEC or FINRA.

That alone makes this case different from many of the other BG Wealth Sharing promoters I have investigated.

Over the past year, I have documented dozens of individuals publicly promoting BG Wealth Sharing through Zoom calls, livestreams, Telegram groups, Facebook pages, BonChat channels and in-person events. Many stayed largely online. Richard and Sumana took things a step further. They became the public face of the opportunity in Utah, creating a physical presence that gave the organisation an appearance of permanence and credibility.

For prospective investors, that physical presence mattered.

People could attend meetings. They could walk into an office. They could meet other members. They could listen to presentations and ask questions face-to-face. In an industry filled with anonymous operators and overseas entities, the existence of local leadership gave many people a sense of comfort. To the average person, a company with offices, events and community leaders naturally appears more trustworthy than one operating entirely through encrypted messaging apps.

The Utah order suggests regulators viewed those activities very differently.

Rather than seeing the office and events as evidence of legitimacy, the Division viewed them as part of a broader recruitment operation designed to attract new investors into BG Wealth Sharing. According to the order, Richard and Sumana were helping organise events, promote the opportunity and build a network of investors throughout Utah while regulators were already examining the operation.

That distinction sits at the heart of this story.

The issue was never whether the office existed.

The issue was whether the investment opportunity being promoted inside that office could withstand scrutiny.

Building The Utah Investor Centre

As I worked through the Utah Division of Securities order, one detail kept standing out.

This was not simply a case of people sharing referral links online or promoting an opportunity through social media. According to regulators, Richard and Sumana Chea helped create a physical BG Wealth presence in Utah, complete with an investor centre, public events and promotional material designed to attract new participants.

That matters because physical offices create trust.

Most people assume that if a company is openly operating from commercial premises, hosting ribbon-cutting ceremonies and inviting the public through its doors, then somebody must have checked whether the business is legitimate. Investors naturally lower their guard when they can see a real office, meet real people and participate in organised events. It creates the impression of stability, transparency and long-term commitment.

According to the Utah order, the Cheas opened an Investor Centre for BG Wealth Utah following a major Salt Lake City event. Regulators allege the facility was then used as a location for recurring meetings and recruitment activities connected to BG Wealth Sharing. Visitors were reportedly encouraged to tour the office and learn more about the opportunity.

The Division’s findings become even more interesting when examining what visitors allegedly saw inside.

According to the order, the office featured framed displays of the same BG Wealth “SEC Certificates” that appeared throughout the company’s marketing materials and online presentations. Regulators allege these certificates were part of a broader effort to create the appearance of regulatory legitimacy. The same documents reportedly appeared in the background of presentations featuring the company’s spokesperson, Professor Stephen Beard, and were repeatedly used to reassure investors that BG Wealth was operating lawfully.

This is where investors need to pay attention.

Many people hear the letters “SEC” and immediately assume a regulator has reviewed the company, approved the business model and verified that everything is operating as advertised. In reality, scammers frequently exploit that assumption by displaying official-looking documents, registrations and filings that sound impressive but do not provide the protections investors believe they do.

The Utah Division specifically alleges that BG Wealth websites depicted fake SEC certificates while claiming authority to manage capital within the United States. Regulators further allege these materials were used to support claims of legitimacy and compliance.

The Investor Centre wasn’t just a meeting place.

According to the order, it also served as a recruitment tool.

Regulators allege that the Cheas distributed printed brochures that closely replicated content from the BG Wealth website. Those brochures reportedly promoted long-term investments, stable income and the promise that members could generate reliable returns by following the guidance of Professor Stephen Beard. The Division notes that these printed materials relied on the same SEC-related representations that appeared elsewhere throughout BG Wealth’s marketing.

Looking back now, the Investor Centre represents one of the most fascinating aspects of the entire BG Wealth story.

The websites were constantly changing.

The domains kept moving.

The leadership remained largely anonymous.

Yet in Utah, investors could walk through the front door of a physical office, shake hands with local promoters and be shown documents that allegedly reinforced the illusion that everything was legitimate.

That combination of physical presence and perceived regulatory credibility may have been one of BG Wealth Sharing’s most effective recruitment tools.

The 2,300-Person Event That Put Utah On The Map

By early 2026, BG Wealth Sharing was no longer operating as a niche online opportunity discussed inside private chat groups and Zoom calls.

The organisation was becoming increasingly ambitious.

Promoters were talking about expansion, leadership growth, regional offices and large-scale public events. The message being delivered to members was clear: BG Wealth Sharing was not shrinking, it was growing. Not only was it growing, but it was supposedly doing so at a pace that critics simply could not understand.

Then came the event that would become one of the most significant milestones in the entire BG Wealth timeline.

According to the Utah Division of Securities, Richard and Sumana Chea organised a major live event in Salt Lake City on April 13, 2026, an event that reportedly attracted approximately 2,300 attendees. The scale alone is remarkable. Most investment opportunities struggle to fill a hotel conference room. BG Wealth Sharing was claiming attendance numbers that rivalled major business conventions.

What makes this event particularly important is not simply the number of people who attended.

It is the timing.

According to the Utah order, the event took place after the Cheas had already received communications from regulators, including investor alert information and notification that their involvement with BG Wealth Sharing was being investigated. The Division further states that the Cheas had been informed of warnings issued by regulators in multiple jurisdictions outside the United States. Despite this, the event proceeded and BG Wealth’s expansion efforts continued.

That creates one of the most important questions in this entire investigation.

What level of due diligence was being performed before encouraging thousands of people to attend these events and potentially invest?

Because by this stage, questions surrounding BG Wealth Sharing were not coming solely from independent investigators, whistleblowers or sceptics online. Regulatory concerns were already beginning to emerge. Yet the public message being delivered to members remained overwhelmingly positive, focused on growth, opportunity and the future of the business.

According to the Utah order, attendees at the Salt Lake City event were treated to a virtual presentation by “Professor Stephen Beard”, the mysterious figure who had become the public face of BG Wealth Sharing. Beard was frequently presented as a highly experienced financial expert with international credentials. However, regulators state they were unable to verify the existence of a person matching the background being promoted to investors.

That alone should have triggered alarm bells.

Whenever an investment opportunity revolves around a central personality, investors should be able to independently verify who that person is, where they worked, what qualifications they hold and whether the claims being made about them are accurate. The deeper investigators looked into Professor Stephen Beard, the more difficult it became to verify the narrative being presented to members.

Yet inside the BG Wealth community, these concerns appeared to have little impact.

The Salt Lake City event became a celebration of growth, momentum and success. To supporters, it appeared to validate everything they had been told. Large crowds create powerful social proof. When hundreds or thousands of people gather together and appear excited about an opportunity, it becomes easier for individuals to silence their doubts and follow the crowd.

That is precisely why these events matter.

They do not simply recruit new investors.

They reinforce belief among existing investors.

Looking back now, the Salt Lake City event may represent the high-water mark of BG Wealth Sharing’s public expansion in the United States. The organisation appeared stronger than ever. The leadership appeared confident. The crowds were growing. The offices were opening.

But beneath the celebrations, regulators were already paying attention.

And the concerns they were documenting would soon become impossible to ignore.

The Regulatory Warnings That Kept Mounting

One of the most common misconceptions investors have when a scheme collapses is that nobody could have seen it coming.

That simply isn’t true.

Long before the Utah Division of Securities issued its Emergency Order, warning signs had already begun appearing around the world. Regulators, investigators, whistleblowers and critics were raising concerns about BG Wealth Sharing while promoters continued assuring members that everything was operating exactly as promised.

I have seen this pattern countless times.

At first, the warnings are dismissed. Supporters claim regulators do not understand cryptocurrency. Critics are labelled negative. Whistleblowers are accused of spreading misinformation. Anyone asking difficult questions is told they are attacking an opportunity that is helping ordinary people achieve financial freedom.

Then more warnings appear.

Then more questions emerge.

Eventually the gap between the public narrative and the available evidence becomes impossible to ignore.

According to the Utah order, regulators specifically noted that Richard and Sumana Chea had been informed about concerns surrounding BG Wealth Sharing and had received information regarding warnings issued by regulatory bodies outside the United States. Despite this, the Division alleges that promotional activities and recruitment efforts continued.

That detail is important because it changes the conversation.

This was no longer a situation where concerns existed only within obscure corners of the internet. By this stage, questions about BG Wealth Sharing had reached government agencies and financial regulators. The concerns were becoming part of the public record.

Yet if you watched many of the promotional presentations being circulated at the time, you would have seen a very different story.

Investors were being shown growth.

Investors were being shown success stories.

Investors were being shown expanding teams, larger events and ambitious plans for the future.

What they were not being shown were the growing concerns surrounding the business model itself.

One of the most troubling aspects of my investigation into BG Wealth Sharing was the way legitimate due diligence questions were often treated as attacks. Questions about Professor Stephen Beard, licensing, trading activity, corporate ownership and regulatory oversight were frequently brushed aside in favour of testimonials and withdrawal screenshots.

But testimonials are not evidence.

A person receiving money from a platform does not prove the underlying business model is legitimate.

A successful withdrawal does not prove profits are coming from external trading activity.

And a growing membership base does not prove an opportunity is sustainable.

History is filled with collapsed investment schemes that paid participants for months or even years before eventually imploding.

That is why regulatory warnings matter.

They force investors to look beyond the excitement, beyond the marketing and beyond the stories being shared inside the community. They force people to ask the questions that promoters often prefer not to answer.

The Utah Division’s findings suggest regulators had reached the point where those unanswered questions could no longer be ignored.

While members continued celebrating growth and expansion, investigators were documenting concerns about unregistered securities, unlicensed activity, alleged misrepresentations and what they ultimately described as a large-scale international cryptocurrency MLM Ponzi operation.

Looking back, the warnings were not isolated incidents.

They were pieces of a larger puzzle.

A puzzle that was becoming increasingly difficult for promoters to explain away.

And at the centre of many of those concerns was a figure that had become synonymous with BG Wealth Sharing itself: Professor Stephen Beard.

The Mystery Of Professor Stephen Beard

Every major investment scheme seems to have a central figure that investors are encouraged to trust.

Sometimes it is a charismatic CEO.

Sometimes it is a celebrity endorsement.

Sometimes it is a successful-looking entrepreneur positioned as the genius behind the operation.

For BG Wealth Sharing, that figure was Professor Stephen Beard.

Throughout the rise of BG Wealth Sharing, Beard was presented as the man behind the success story. Investors were told he possessed extensive financial expertise. He appeared in presentations, webinars and promotional material. His image appeared throughout the organisation’s marketing, and members were encouraged to believe they were benefiting from the knowledge and experience of a seasoned financial professional.

The problem was that the deeper I looked, the harder it became to independently verify who he actually was.

That should concern every investor.

When somebody is being presented as the driving force behind an investment opportunity handling millions of dollars in investor funds, basic due diligence should be straightforward. There should be a verifiable employment history. Professional credentials should be easy to confirm. Public records should support the claims being made. Independent sources should be able to verify the person’s background.

Yet throughout my investigation, those questions remained largely unanswered.

According to the Utah Division of Securities, Professor Stephen Beard was promoted as a British national who had previously worked for the International Monetary Fund (IMF). That claim carried enormous weight inside the BG Wealth community because it created the impression that investors were being guided by someone with genuine international financial expertise. However, regulators state that their investigation found no such person with a verifiable affiliation to the IMF.

That finding strikes at the heart of BG Wealth Sharing’s credibility.

Because if investors were persuaded to trust the platform based on Beard’s alleged expertise, then the obvious question becomes: who exactly were they trusting?

This is where the story becomes even more unusual.

Many members never met Professor Stephen Beard in person. Instead, they were introduced to him through carefully produced presentations, videos and online appearances. As time went on, increasing questions emerged regarding whether Beard was even a real individual or simply a character being used to front the operation. Critics raised concerns. Whistleblowers raised concerns. Investigators raised concerns.

Yet inside the BG Wealth community, questioning Beard often attracted the same response as questioning the company itself.

People were told to focus on results.

People were told to look at their account balances.

People were told to stop being negative.

But credibility is not established by account balances on a screen. Credibility comes from transparency, verification and evidence.

The Utah order also notes that the same fake SEC certificates allegedly used to create legitimacy around BG Wealth Sharing frequently appeared in the background of Beard’s presentations. According to regulators, these materials formed part of a broader effort to portray BG Wealth as operating with regulatory approval and authority that the Division alleges did not exist.

Looking back, one of the most remarkable aspects of the BG Wealth story is how much trust was placed in a man who appears to have left so little verifiable evidence of his existence.

Thousands of investors deposited money.

Thousands of investors followed instructions.

Thousands of investors believed they were participating in a sophisticated trading operation led by an experienced financial professional.

Yet regulators now say they were unable to verify one of the central claims used to establish that credibility in the first place.

That should serve as a powerful lesson for anyone considering any investment opportunity.

Before trusting the promises, verify the people making them.

Because if the person at the centre of the story cannot withstand basic due diligence, the rest of the story deserves much closer scrutiny as well.

The Fake SEC Certificates And The Illusion Of Legitimacy

If there is one lesson investors should take away from the BG Wealth Sharing story, it is that official-looking paperwork is not the same thing as regulatory approval.

Throughout my investigation, I repeatedly encountered promoters pointing to documents, registrations and certificates as proof that BG Wealth Sharing was legitimate. Whenever concerns were raised about the company, the trading activity or the leadership, supporters often responded by producing screenshots of filings and certificates that appeared to show the business was recognised by government authorities.

To the average investor, that can be incredibly persuasive.

Most people do not spend their time studying securities law. They see the letters “SEC” and assume that a regulator has reviewed the company, approved its operations and confirmed that everything is above board. That assumption creates a dangerous shortcut in the decision-making process because it encourages people to stop asking questions.

According to the Utah Division of Securities, that trust may have been misplaced.

The Division alleges that BG Wealth websites displayed fake “SEC Certificates” and represented that BG Wealth had authority to manage capital within the United States under federal law. Regulators further allege that copies of entity filings and related documentation were used to create the appearance of legitimacy and regulatory compliance.

That allegation is significant because it strikes directly at one of the most effective marketing tools available to any investment scheme: borrowed credibility.

Fraudulent investment opportunities rarely tell investors, “Trust us because we are unregulated.” Instead, they attempt to associate themselves with respected institutions, government agencies, regulatory bodies and legal frameworks. The goal is simple. If investors believe regulators have already done the hard work of verifying the business, they are less likely to perform due diligence themselves.

According to the Utah order, these certificates did not just appear on websites.

Regulators allege that the same materials appeared in the background of Professor Stephen Beard’s presentations and were displayed inside the Utah Investor Centre. Visitors walking into the office were reportedly exposed to the same imagery and representations that had already been circulating online.

When viewed in isolation, a certificate hanging on a wall may seem insignificant.

But when combined with a physical office, large public events, an internationally promoted spokesperson and thousands of enthusiastic members, the effect becomes far more powerful. Each piece reinforces the others. The office appears to validate the certificates. The certificates appear to validate the company. The company appears to validate the promoters. And the promoters appear to validate the opportunity.

That is how legitimacy is manufactured.

Not through transparency.

Not through independently audited financial records.

Not through verifiable trading performance.

But through a carefully constructed collection of visual signals that encourage investors to believe somebody else has already done the verification for them.

One of the most frustrating aspects of investigating schemes like BG Wealth Sharing is watching investors mistake paperwork for proof.

A filing is not proof of profitability.

A registration is not proof of legitimacy.

A certificate is not proof that trading is occurring.

And a document displayed on a wall is certainly not proof that investor funds are safe.

The Utah Division ultimately concluded that the representations surrounding these certificates formed part of a broader pattern of conduct that warranted emergency intervention. The order alleges that investors were being presented with a false impression of regulatory approval while continuing to be recruited into the opportunity.

Looking back now, the fake SEC certificates were not a side issue.

They were one of the pillars supporting the entire illusion.

Because if investors stopped believing the company was regulated, they would inevitably start asking the questions that mattered most.

Where was the trading?

Who controlled the money?

And if the regulators had never approved any of this, why were people being told they had?

Where Were The Trading Profits Coming From?

Every investment opportunity eventually comes down to one simple question:

Where is the money coming from?

It is the question that cuts through the marketing, the testimonials, the excitement and the promises. It is also the question that many BG Wealth Sharing promoters seemed reluctant or unable to answer with independently verifiable evidence.

Throughout the rise of BG Wealth Sharing, investors were told their profits were being generated through sophisticated cryptocurrency trading. Members followed daily signals, watched account balances increase and were encouraged to believe that a team of experienced traders was producing consistent returns on their behalf. The entire business model rested on the idea that external trading activity was generating enough revenue to support the withdrawals, bonuses and growth being celebrated throughout the organisation.

The problem is that regulators say they could not find evidence supporting that narrative.

According to the Utah Division of Securities, there was no evidence of actual trading activity taking place behind the scenes. Instead, regulators allege that BG Wealth Sharing and DSJ Exchange deployed a constantly shifting network of websites and domains while presenting investors with simulated account growth. The order states that respondents used at least 39 different URLs as part of the operation while allegedly attempting to evade regulatory scrutiny and maintain the appearance of a functioning investment platform.

That finding is absolutely critical.

Because if legitimate trading profits were not generating the returns being displayed inside investor accounts, then those returns had to be coming from somewhere else.

This is where many investors become confused.

People often point to successful withdrawals as proof that a platform is legitimate. I have heard this argument hundreds of times over the years. Somebody withdraws money, receives a payment and immediately concludes that the business model must be genuine. The reality is very different. Early withdrawals are often one of the most effective recruitment tools available to any investment scheme because they create confidence and encourage participants to invest more money and recruit others.

A withdrawal proves only one thing.

It proves somebody received money.

It does not prove where that money originated.

Throughout my investigation into BG Wealth Sharing, I repeatedly asked promoters for evidence of real trading activity. Not screenshots. Not account balances. Not testimonials. Actual evidence showing that external trading revenue existed at a scale capable of supporting the returns being advertised.

Those questions rarely received satisfactory answers.

Instead, conversations often drifted back to personal success stories, community growth, lifestyle achievements and examples of people who had successfully withdrawn funds. While those stories may have been genuine experiences, they did not explain the underlying source of revenue driving the system.

The Utah order paints a picture that should concern every investor who participated in BG Wealth Sharing.

Regulators allege that the operation used rapidly changing websites, simulated asset growth and fabricated legitimacy while continuing to recruit new investors. If those allegations are correct, then the numbers people were watching on their screens may have reflected little more than an illusion designed to encourage confidence and continued participation.

Looking back, the most revealing aspect of BG Wealth Sharing was not the promises being made.

It was the lack of independently verifiable evidence supporting those promises.

Because if a company is genuinely generating extraordinary profits through trading, proving it should be relatively straightforward.

When proving it becomes impossible, investors should start asking why.

And by the time regulators reached their conclusions, those unanswered questions had become impossible to ignore.

The Collapse, The 12% Fee And The HQI Exchange Escape Plan

For months, BG Wealth Sharing promoters reassured investors that everything was working exactly as intended.

Members were encouraged to trust the process, follow the signals and remain patient. Account balances continued to grow on-screen. Recruitment continued. Events continued. Public confidence remained high.

Then the cracks started to appear.

As withdrawal problems began surfacing, the narrative surrounding BG Wealth Sharing started to change. Investors who had previously been told that their funds were secure suddenly found themselves facing delays, restrictions and growing uncertainty. Questions that had once been dismissed as negativity became increasingly difficult to avoid.

What happened next should concern anyone who studies investment fraud.

Rather than providing transparent explanations supported by independently verifiable evidence, investors were presented with new obstacles that allegedly needed to be overcome before they could access their money. One of the most controversial developments involved demands that members pay what became widely known throughout the community as a 12% fee or 12% tax before funds could be released.

The explanation changed depending on who was telling the story.

Some investors were told the payment was required for tax purposes. Others were told it was part of a compliance process. Different explanations circulated throughout BonChat groups, livestreams and private discussions. What remained consistent was the message that investors needed to send additional money before they could recover the funds they believed already belonged to them.

That is a major red flag.

Legitimate financial institutions do not typically require customers to send money upfront in order to access money they already own. Whenever an investment platform begins demanding additional payments before withdrawals can occur, investors should immediately pause and ask why.

Unfortunately, the situation became even more concerning.

According to the Utah Division of Securities, investors who had already lost access to their funds were subsequently directed toward a new platform called HQI Exchange. Regulators allege that respondents attempted to sustain the operation by routing victims to the new platform while simultaneously promoting what the Division describes as a secondary advance-fee scheme requiring investors to pay an additional $100 migration fee in order to recover their balances.

This is where the story starts to look remarkably familiar to anyone who has investigated collapsed investment schemes before.

When confidence in one platform disappears, another platform suddenly emerges.

When withdrawals become impossible, a recovery solution appears.

When investors begin losing faith, they are offered one final opportunity to save their investment.

The names change.

The websites change.

The branding changes.

But the underlying story often remains exactly the same.

The Utah order suggests regulators were looking at the entire sequence of events rather than viewing each development in isolation. Investigators specifically reference the transition from BG Wealth Sharing and DSJ Exchange to HQI Exchange, alleging that the migration was being used to continue soliciting investors despite growing regulatory scrutiny and widespread public warnings.

For many victims, this was the moment everything finally unraveled.

The promises of financial freedom had become demands for additional payments.

The confidence of earlier presentations had been replaced with explanations, delays and migration instructions.

The platform that was supposedly generating extraordinary trading profits now required investors to jump through increasingly complicated hoops simply to access their own money.

Looking back, the collapse of BG Wealth Sharing was not defined by a single event.

It was defined by a series of escalating explanations designed to keep investors believing for just a little longer.

First came the trading story.

Then came the withdrawal delays.

Then came the 12% payment demands.

Then came HQI Exchange.

And eventually, even that solution collapsed under the weight of its own unanswered questions.

By the time the Utah Division of Securities issued its Emergency Order, regulators had reached a stark conclusion: investors were facing what the Division described as an ongoing advance-fee scheme that continued exposing victims to further financial harm.

For many investors, that warning arrived far too late.

But it finally put into writing what critics, whistleblowers and victims had been saying for months.

The problem was never the platform.

The problem was the story investors had been told to trust.

Utah Regulators Finally Step In

For months, critics were told they did not understand BG Wealth Sharing.

Victims were told to trust the process.

Promoters insisted withdrawals would resume, problems would be resolved and the future remained bright.

Then the Utah Division of Securities stepped in.

On June 1, 2026, the Division issued an Emergency Order to Cease and Desist against BG Wealth Sharing Ltd, BG Wealth Sharing Ltd. Liability Company, DSJ Exchange Pty Ltd, HQI Exchange, Richard Chea and Sumana Chea. The order was not a routine warning or investor alert. It was an emergency enforcement action issued because regulators concluded that immediate intervention was necessary to protect the public.

That distinction is important.

Regulators do not typically invoke emergency powers simply because an investment opportunity is controversial. Emergency actions are reserved for situations where authorities believe there is an ongoing threat of financial harm. In this case, the Division concluded that the respondents’ activities presented what it described as a “grave, continuous threat of irreparable financial ruin” to investors.

That is extraordinarily strong language.

After reviewing the order, what struck me most was the scope of the allegations.

This was not simply a complaint about a missing licence or a technical regulatory violation. The Division alleges that respondents were operating a large-scale international cryptocurrency MLM Ponzi and advance-fee fraud scheme that targeted Utah residents and investors around the world. Regulators further allege that investors were being lured through promises of compounding daily returns, misleading regulatory claims and aggressive recruitment efforts.

The order also paints a picture of an organisation that regulators believed was actively adapting in an attempt to stay ahead of scrutiny.

According to the Division, BG Wealth Sharing and its related entities used rapidly changing domains, shifting platforms and evolving narratives while continuing to solicit new participants. Regulators allege that even after public warnings emerged and concerns intensified, recruitment activities continued through local events, promotional meetings and the Utah Investor Centre.

For Richard and Sumana Chea, this is where the story becomes particularly significant.

The order does not merely mention them in passing.

It specifically identifies them as respondents and details what regulators allege was their role in promoting BG Wealth Sharing within Utah. According to the Division, the couple acted as local agents, managers and recruiters while helping establish a visible physical presence for the organisation. The order further references the Salt Lake City event, the Investor Centre, promotional materials and continued recruitment efforts despite growing regulatory concerns.

That raises a question every investor should be asking.

At what point does a promoter stop being someone who simply believed in an opportunity and become someone who bears responsibility for continuing to promote it?

That question is ultimately for regulators, courts and investigators to determine.

What we do know is that the Utah Division believed the situation had reached a point where immediate action was required.

The cease and desist order directed respondents to immediately stop offering or selling investments, stop marketing or recruiting for BG Wealth Sharing, DSJ Exchange and HQI Exchange, stop contacting investors and cease further violations of Utah securities law. The order also warned that violating the directive could expose respondents to additional legal consequences, including criminal penalties under Utah law.

Perhaps the most remarkable aspect of the order is how closely it mirrors many of the concerns that critics, whistleblowers and victims had been raising for months.

Questions about Professor Stephen Beard.

Questions about the trading.

Questions about the regulatory claims.

Questions about the recruitment.

Questions about the movement from DSJ Exchange to HQI Exchange.

Questions about why investors were being asked to send additional money.

The difference now is that those questions are no longer being asked solely by sceptics on the internet.

They are being documented by a government securities regulator.

And that changes everything.

Richard Chea’s Response And The Questions That Remain

One of the advantages of documenting investigations as they unfold is that eventually people have an opportunity to respond.

That is important.

Too often, supporters of failed schemes claim that critics never sought their side of the story or ignored information that did not fit a predetermined narrative. I have never believed that accountability and fairness are mutually exclusive. If somebody wishes to explain their actions, provide additional context or challenge factual claims, they should be given that opportunity.

According to reporting by BehindMLM—and a tip of the hat to Oz for his research—Richard Chea responded after the Utah Division of Securities issued its Emergency Order.

In his response, Chea reportedly stated:

“Without admitting any wrongdoing or liability, I have reviewed your claims and have taken steps to comply with your requests.”

He further stated that the referenced activity had been discontinued, related materials had been removed or disabled, and that he would ensure no future actions occurred that violated the concerns outlined by regulators.

On the surface, that may sound reassuring.

The problem is that by the time those statements were made, BG Wealth Sharing had already collapsed, DSJ Exchange had already failed, and HQI Exchange had already become the latest attempted solution for frustrated investors.

The real questions are not about what happened after the collapse.

The real questions are about what happened before it.

Those are the questions victims deserve answers to.

For example, when exactly did Richard and Sumana become aware of the concerns surrounding BG Wealth Sharing?

When did they first learn about regulatory warnings being issued in multiple jurisdictions?

What due diligence was performed regarding Professor Stephen Beard and the claims being made about his professional background?

What evidence were they shown that convinced them the advertised trading activity was genuine?

And perhaps most importantly, what steps were taken to independently verify the source of the returns being displayed inside investor accounts?

These are not unreasonable questions.

They are the same questions any responsible investor should ask before entrusting money to an investment opportunity.

They are also the same questions promoters should be asking before encouraging others to participate.

The Utah Division’s order suggests regulators believed these concerns were serious enough to justify emergency intervention. Yet many investors were still being encouraged to trust the process, attend events, visit the Investor Centre and continue believing that solutions were just around the corner.

Another important question concerns the transition from BG Wealth Sharing to HQI Exchange.

Who approved that migration?

What due diligence was performed before investors were directed toward another platform?

Why were members being encouraged to send additional funds if the underlying problem had supposedly been caused by external circumstances?

And what evidence existed that HQI Exchange would succeed where BG Wealth Sharing and DSJ Exchange had failed?

These questions remain largely unanswered.

That does not automatically mean every promoter knowingly participated in wrongdoing.

What it does mean is that good intentions alone are not enough.

Throughout my investigations over the years, I have encountered many people who genuinely believed they were helping others while promoting opportunities that later collapsed. Some made money. Some lost money. Some became victims themselves. But regardless of intent, the consequences remain the same when ordinary people are encouraged to place trust in a system that cannot withstand scrutiny.

The reality is that many victims are no longer interested in motivational speeches, explanations or reassurances.

They want facts.

They want accountability.

They want transparency.

And they want to know how an opportunity that was promoted so aggressively, defended so passionately and celebrated so publicly ended with regulators issuing emergency enforcement actions and investors struggling to recover their money.

Those are the questions that still need answers.

And they are not going away simply because the websites have disappeared.

The Wider Network Of BG Wealth Sharing Promoters

One of the reasons BG Wealth Sharing was able to spread so rapidly is that it was never promoted by just one or two people.

Like many MLM-style investment schemes before it, the operation relied on a growing network of recruiters, influencers, team builders and community leaders who encouraged others to participate. Some hosted Zoom meetings. Some ran Facebook groups. Some organised local events. Others conducted one-on-one presentations, shared withdrawal screenshots or reassured nervous investors whenever concerns emerged.

While the Utah Division of Securities specifically named Richard Chea and Sumana Chea in its Emergency Order, they were far from the only individuals publicly promoting BG Wealth Sharing.

Over the course of my investigation, I archived videos, recorded livestreams, collected screenshots, monitored social media activity and reviewed countless hours of promotional content. Through that process, I observed a much wider network of individuals publicly supporting, promoting or defending BG Wealth Sharing, DSJ Exchange, HQI Exchange or related migration efforts.

It is important to be clear about what this means.

The individuals listed below are not being identified here as respondents in the Utah action unless specifically named by regulators. Their inclusion simply reflects that they were publicly observed promoting, recruiting for, defending or encouraging participation in BG Wealth Sharing at various stages of its growth and eventual collapse.

That distinction matters.

Being observed promoting an opportunity is not the same thing as being accused by regulators of wrongdoing.

However, when thousands of investors lose money, it is entirely reasonable for the public to examine who helped promote the opportunity, what claims were being made and whether those claims were supported by evidence at the time.

Among the individuals publicly associated with the promotion of BG Wealth Sharing were:

Gagan Sarkaria, Jimmie Williams, Arlene Williams, Vida Frean, Linda Meadors, Milton Chisom, Natasha Sepetaio, Xiaoan Lin, Keith Darren Hudson, Cynthia Tran, Tu Tran, Bud Ayers, Ben Acorda, Laie Namoa Laakulu, Janessa A. Morgan, Nee Barton, Bridgette M. Farris, Carl D. Farris, Earl Stringer, Brian N. Beane, Mahbub Hossain, Gaurang Gary Bhatt, Shamim Hossain, Cornelius Jones, Bronson Salcedo, Nilda Greschner, Richard Chea, Sumana Chea, Coach Curtis, Mark Baker, Kenneth Lampkins, Lee Meadows, Emmanuel Bernstein, Marcus Smith, Angela Smith, Loaloa Wily-Afo, Binod Ray, Thaddious Thomas, Faiana Brown, Don Williams, Anne-Marie Lerch, Mark Brown, Kim Brown, Anthony Bryant, Anh Pham, Jossie G. Gallizia, Denise Ayso, Monica Hussain, Mesam Raza Jiwani, Steven Rachel, Latanya Jones-Kerr, Drew Burton, Arthur Bankston Jr., Dawn Keeler, Bill Keeler, Chanse Carlson, Randy Crosby, Sonya Crosby, Oliver Sagala and Yitzhak Morrison.

Some of these individuals appeared repeatedly in recruitment meetings. Some built substantial teams. Some hosted events. Others played a more limited role. In many cases, I observed promoters assuring members that concerns surrounding BG Wealth Sharing were overblown, temporary or the result of misinformation being spread by critics.

That is why documentation matters.

When an opportunity is thriving, promoters are often proud to publicly associate themselves with it. They celebrate growth, share success stories and encourage others to join. When the opportunity collapses, however, the narrative frequently changes. Videos disappear. Social media posts are removed. Websites vanish. Explanations evolve.

The public record becomes incredibly important during that transition.

That is one reason I archive presentations, preserve recordings and collect evidence while events are unfolding. Not because I expect every promoter to have acted dishonestly, but because memories become unreliable once money is lost and difficult questions start being asked.

The reality is that BG Wealth Sharing did not grow because of websites alone.

It grew because people promoted it.

People defended it.

People reassured others that it was safe.

People encouraged friends, family members and community members to trust it.

And as regulators continue investigating the wider operation, it would not be surprising if additional questions are asked about the roles various promoters played in helping the organisation expand throughout the United States and beyond.

Whether any further regulatory action emerges remains to be seen.

What is already clear is that the story of BG Wealth Sharing is far larger than any single website, exchange or AI-generated spokesperson.

It is also the story of the people who helped bring the opportunity to the public.

The Questions Victims Still Deserve Answered

As I finish writing this article, I keep coming back to the same thought.

The biggest tragedy in the BG Wealth Sharing story is not the websites that disappeared, the exchanges that failed or the regulatory actions that followed.

The biggest tragedy is the people who trusted what they were being told.

Many investors did not discover BG Wealth Sharing through a random advertisement on the internet. They joined because somebody they knew recommended it. A friend. A family member. A church member. A business associate. Someone they respected. Someone who appeared confident. Someone who assured them that the opportunity had been researched and that the risks had been understood.

That trust is incredibly difficult to rebuild once it has been broken.

Today, many of those investors are left with far more questions than answers. They want to know where their money went. They want to know who controlled the funds. They want to know whether any real trading ever took place. They want to understand why concerns raised by critics, whistleblowers and regulators were repeatedly dismissed while recruitment efforts continued to accelerate.

The Utah Division of Securities has now documented many of the same concerns that victims and investigators were raising months earlier. Regulators allege that BG Wealth Sharing, DSJ Exchange, HQI Exchange and associated respondents were involved in a scheme that exposed investors to significant financial harm. The Emergency Order represents one of the most serious regulatory actions taken against the operation to date.

Yet despite the government’s intervention, many questions remain unanswered.

How much money flowed into BG Wealth Sharing?

How much was paid out?

Who ultimately controlled the wallets and accounts?

What happened to the funds investors believed were being traded?

How much money was earned through recruitment commissions and bonuses?

Who approved the transition from DSJ Exchange to HQI Exchange?

And what due diligence was performed before thousands of people were encouraged to trust the system?

These are not questions motivated by revenge.

They are questions motivated by accountability.

Because accountability is not about punishing people for being wrong. It is about understanding what happened, documenting the evidence and ensuring the same mistakes are not repeated.

Throughout my investigation, I archived videos, recorded presentations, saved websites and documented the claims being made as events unfolded. I did so because experience has taught me that evidence becomes increasingly valuable after a collapse. Websites disappear. Social media posts are deleted. Explanations change. Memories fade.

The receipts do not.

Looking back now, the warning signs were there.

Questions about Professor Stephen Beard were there.

Questions about the trading were there.

Questions about the SEC certificates were there.

Questions about recruitment were there.

Questions about the constant domain changes were there.

Questions about withdrawals were there.

Questions about the 12% payment demands were there.

Questions about HQI Exchange were there.

The problem was never a lack of warning signs.

The problem was that too many people were encouraged to ignore them.

For Richard Chea, Sumana Chea and the wider network of promoters who publicly supported BG Wealth Sharing, the Utah action represents a turning point. For months, the conversation revolved around growth, opportunity and financial freedom. Today, the conversation revolves around regulatory findings, investor losses and unanswered questions.

Whether further enforcement actions follow remains to be seen.

Whether additional promoters find themselves under regulatory scrutiny remains to be seen.

Whether victims ever recover their money remains to be seen.

But one thing is already certain.

The story of BG Wealth Sharing is no longer being written by promoters.

It is being written by victims, investigators, regulators and the evidence itself.

And long after the websites disappear, the domains expire and the marketing stops, that evidence will remain.

Because the truth has a habit of surviving long after the hype is gone.

Disclaimer: How This Investigation Was Conducted

This investigation relies entirely on OSINT — Open Source Intelligence — meaning every claim made here is based on publicly available records, archived web pages, corporate filings, domain data, social media activity, and open blockchain transactions. No private data, hacking, or unlawful access methods were used. OSINT is a powerful and ethical tool for exposing scams without violating privacy laws or overstepping legal boundaries.

About the Author

I’m DANNY DE HEK, a New Zealand–based YouTuber, investigative journalist, and OSINT researcher. I name and shame individuals promoting or marketing fraudulent schemes through my YOUTUBE CHANNEL. Every video I produce exposes the people behind scams, Ponzi schemes, and MLM frauds — holding them accountable in public.

My PODCAST is an extension of that work. It’s distributed across 18 major platforms — including Apple Podcasts, Spotify, Amazon Music, YouTube, and iHeartRadio — so when scammers try to hide, my content follows them everywhere. If you prefer listening to my investigations instead of watching, you’ll find them on every major podcast service.

You can BOOK ME for private consultations or SPEAKING ENGAGEMENTS, where I share first-hand experience from years of exposing large-scale fraud and helping victims recover.

“Stop losing your future to financial parasites. Subscribe. Expose. Protect.”

My work exposing crypto fraud has been featured in:

- Coffeezilla 2026): Featured in the investigation exposing the alleged $328M Goliath Ventures Ponzi scheme

- Bloomberg Documentary (2025): A 20-minute exposé on Ponzi schemes and crypto card fraud

- News.com.au (2025): Profiled as one of the leading scam-busters in Australasia

- OpIndia (2025): Cited for uncovering Pakistani software houses linked to drug trafficking, visa scams, and global financial fraud

- The Press / Stuff.co.nz (2023): Successfully defeated $3.85M gag lawsuit; court ruled it was a vexatious attempt to silence whistleblowing

- The Guardian Australia (2023): National warning on crypto MLMs affecting Aussie families

- ABC News Australia (2023): Investigation into Blockchain Global and its collapse

- The New York Times (2022): A full two-page feature on dismantling HyperVerse and its global network

- Radio New Zealand (2022): “The Kiwi YouTuber Taking Down Crypto Scammers From His Christchurch Home”

- Otago Daily Times (2022): A profile on my investigative work and the impact of crypto fraud in New Zealand

Leave A Comment