“I merely did what I was asked to do and paid to do.”

— Harry M Samuels

Administrative Distance Under Federal Scrutiny

When a corporate structure collapses under federal criminal charges, scrutiny does not stop with the founder. It expands outward — to the professionals who formed the entities, filed the paperwork, prepared the tax returns, and maintained the administrative framework.

On February 20, 2026, a federal criminal complaint was filed in the United States District Court for the Middle District of Florida charging Christopher Alexander Delgado with:

- 18 U.S.C. § 1343 – Wire Fraud

- 18 U.S.C. § 1957 – Money Laundering

(See page 1 of the federal criminal complaint .)

The affidavit summary states that GOLIATH allegedly operated as a Ponzi scheme and that at least $328 million was obtained from investors through materially false representations .

Against this backdrop, Harry M Samuels — accountant and former Registered Agent connected to Goliath Ventures Inc — has confirmed he is resigning from all Delgado-related entities.

This article does not allege criminal conduct by Mr. Samuels. It examines:

- His written explanations

- Public corporate filings

- The timing of jurisdictional shifts

- His firm’s advertised service scope

- The professional overlap involving Nadia Bringas

- The confirmed federal criminal complaint

The filings are public.

The complaint is federal.

The resignation is confirmed.

The question is whether the explanation of “minimal administrative involvement” aligns with the broader factual record.

What Harry M Samuels Says His Role Was

In correspondence, Mr. Samuels consistently described his involvement as limited and administrative. He stated:

“I was not involved in any planning or enterprise structuring.”

“I prepared the tax returns from documentation provided to me.”

“Registered Agents are not required to do any further due diligence.”

“I merely did what I was asked to do and paid to do.”

He maintains that:

- He formed entities upon request.

- He acted as Registered Agent.

- He prepared tax returns from reconciled books.

- He did not audit operations.

- He did not verify business practices.

He has now confirmed he is resigning as both Registered Agent and accountant for Mr. Delgado and related entities.

That is his position. It is important to present it accurately.

The Federal Criminal Complaint Against Goliath

The federal complaint alleges that from January 2023 through January 2026, GOLIATH solicited investor funds under representations that money would be deployed into cryptocurrency “liquidity pools.” Instead, the complaint alleges:

- Investor funds were primarily used to pay earlier investors.

- Funds were not deployed into liquidity pools as represented.

- Investor portals displayed misleading or fabricated returns.

- Substantial sums were used for personal real estate purchases.

- Approximately $328 million was obtained from victims.

These findings are contained in the sworn affidavit supporting the complaint .

These are federal allegations establishing probable cause, not trial verdicts. However, they materially change the context in which professional proximity is examined.

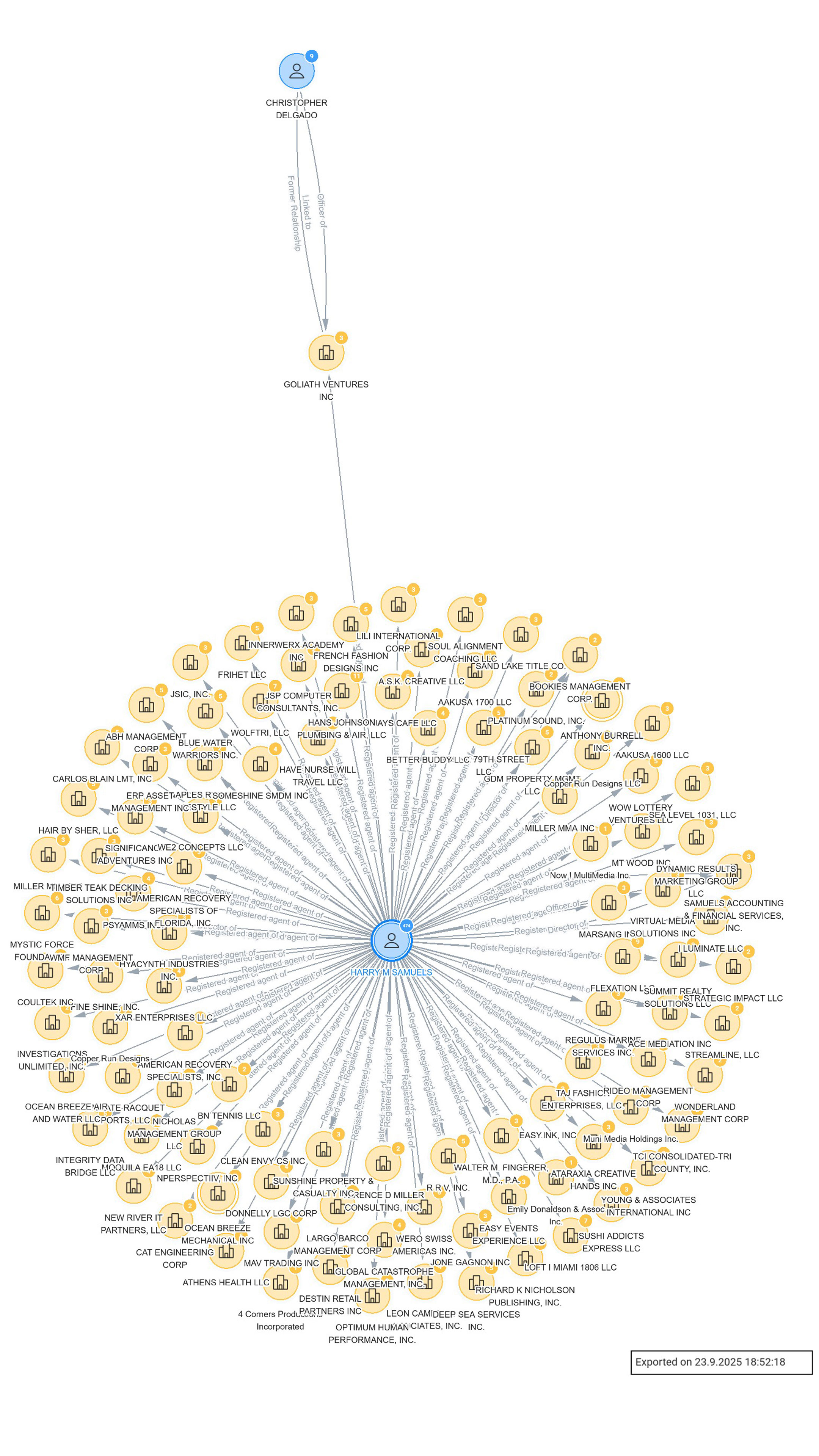

The Scale of the Corporate Network

Public filings show a large interconnected entity network tied to Christopher Delgado and Goliath Ventures Inc. Across many filings, Harry M Samuels appears in roles such as:

- Formation filer

- Registered Agent

- Compliance contact

- Tax preparer

The accompanying corporate graphic illustrates the breadth and density of this network.

Scale alone does not establish wrongdoing.

However, when dozens — potentially hundreds — of entities are formed within a tightly connected structure, legitimate questions arise:

- Why were so many entities created?

- What business function did each serve?

- Were they operational, dormant, or speculative?

Mr. Samuels has stated many entities were formed for future ventures or unspecified purposes. That explanation is now documented.

The Public Record: Entities Associated Through Filings

The accompanying corporate graphic was generated using commercial entity-linking software that maps relationships drawn from publicly available state filings. The visualisation reflects entities in which Harry M Samuels appears in administrative capacities — including Registered Agent, formation contact, officer, or filing representative — based solely on documented public records.

This graphic does not assert that all listed entities are connected to Goliath Ventures Inc, nor does it allege misconduct by unrelated businesses or individuals. It illustrates structural proximity through shared administrative roles appearing in state filings.

The purpose of including the graphic is to demonstrate scale and repetition — specifically, the volume of entities in which the same administrative contact appears — and to provide context for readers assessing the broader corporate environment in which Goliath Ventures Inc operated.

The recurring appearance of the same administrative contact across such a dense filing network is notable. However, inclusion in the visual map does not imply involvement in, or connection to, the Goliath matter.

Readers are encouraged to review the underlying public filings independently.

The September 2–3 Corporate Shift

The September 2–3 Corporate Shift

On September 2, 2025, BRINGAS BOOKKEEPING CORP was filed in Wyoming.

On September 3, 2025, GOLIATH VENTURES INC was filed in Wyoming.

Both had previously operated in Florida. Both transitioned jurisdictions within approximately 24 hours. Both filings include Harry’s email in the documentation. Both list Hubco Registered Agent Services in Wyoming.

Companies relocate for legitimate reasons. However, the tight synchronization between the bookkeeping entity and the primary operating entity — shortly before public collapse — is part of the factual record.

Mr. Samuels states he was not involved in planning or restructuring. The filings show his contact information present during this transition.

That timing is documented. Interpretation is left to readers.

Nadia Bringas: Staff Member and Independent Operator

Screenshots from Mr. Samuels’ website (captured today) show Nadia Bringas listed as part of his accounting team.

At the same time:

- She operated BRINGAS BOOKKEEPING CORP independently.

- That company shifted to Wyoming within the same 24-hour period as Goliath.

- She appeared at Goliath conferences.

- Mr. Samuels confirms she previously worked for him and occasionally assists his firm.

This creates a documented professional overlap:

- Website staff listing

- Independent bookkeeping corporation

- Conference appearances

- Tax return preparation based on reconciled books

This does not establish wrongdoing. It demonstrates proximity.

Service Scope vs Claimed Involvement

Mr. Samuels’ website advertises services including:

- GAAP-formatted financial statements

- Attest services

- Cash flow analysis

- Forensic accounting

- Consulting services

- Tax planning

- IRS representation

These services often involve analysis and review.

In correspondence, however, he maintains his work with Goliath was strictly limited to preparing tax returns from client-provided documentation and not operational review.

There is a distinction between services offered and services provided.

The question readers may ask is whether the involvement with Goliath was truly limited to mechanical compliance — or whether advisory and bookkeeping functions were intertwined.

Mr. Samuels maintains they were not.

The Resignation

Mr. Samuels has confirmed he is resigning as Registered Agent and accountant for Mr. Delgado and related entities.

He states:

“Morally and ethically, I want nothing to do with businesses or individuals involved in any type of criminal enterprise, whether alleged or proven.”

Resignation does not imply guilt. Professionals withdraw for many reasons — insurance considerations, reputational protection, legal advice.

However, resignation after federal charges inevitably raises timing questions.

If involvement was strictly administrative and compliant, why withdraw now?

That question is chronological, not accusatory.

Professional Distance vs Professional Responsibility

There is a legal distinction between liability and proximity.

A Registered Agent is not automatically responsible for a client’s actions.

A tax preparer is not required to audit every transaction.

But when a professional appears across a dense entity network, participates in filings during synchronized jurisdictional shifts, prepares tax returns from internal books, and employs or associates with the company’s bookkeeper — the public will examine context.

Mr. Samuels has asked that his role be clarified. It has been clarified here using:

- His written statements

- Public corporate records

- Federal court filings

He formed entities.

He acted as Registered Agent.

He prepared tax returns from client-provided documentation.

He did not audit operations.

He is now resigning.

The federal charges are public .

The structure is visible.

The timing is documented.

The remaining questions are structural — not accusatory.

Readers can assess the record for themselves.

Disclaimer: How This Investigation Was Conducted

This investigation relies entirely on OSINT — Open Source Intelligence — meaning every claim made here is based on publicly available records, archived web pages, corporate filings, domain data, social media activity, and open blockchain transactions. No private data, hacking, or unlawful access methods were used. OSINT is a powerful and ethical tool for exposing scams without violating privacy laws or overstepping legal boundaries.

About the Author

I’m DANNY DE HEK, a New Zealand–based YouTuber, investigative journalist, and OSINT researcher. I name and shame individuals promoting or marketing fraudulent schemes through my YOUTUBE CHANNEL. Every video I produce exposes the people behind scams, Ponzi schemes, and MLM frauds — holding them accountable in public.

My PODCAST is an extension of that work. It’s distributed across 18 major platforms — including Apple Podcasts, Spotify, Amazon Music, YouTube, and iHeartRadio — so when scammers try to hide, my content follows them everywhere. If you prefer listening to my investigations instead of watching, you’ll find them on every major podcast service.

You can BOOK ME for private consultations or SPEAKING ENGAGEMENTS, where I share first-hand experience from years of exposing large-scale fraud and helping victims recover.

“Stop losing your future to financial parasites. Subscribe. Expose. Protect.”

My work exposing crypto fraud has been featured in:

- Bloomberg Documentary (2025): A 20-minute exposé on Ponzi schemes and crypto card fraud

- News.com.au (2025): Profiled as one of the leading scam-busters in Australasia

- OpIndia (2025): Cited for uncovering Pakistani software houses linked to drug trafficking, visa scams, and global financial fraud

- The Press / Stuff.co.nz (2023): Successfully defeated $3.85M gag lawsuit; court ruled it was a vexatious attempt to silence whistleblowing

- The Guardian Australia (2023): National warning on crypto MLMs affecting Aussie families

- ABC News Australia (2023): Investigation into Blockchain Global and its collapse

- The New York Times (2022): A full two-page feature on dismantling HyperVerse and its global network

- Radio New Zealand (2022): “The Kiwi YouTuber Taking Down Crypto Scammers From His Christchurch Home”

- Otago Daily Times (2022): A profile on my investigative work and the impact of crypto fraud in New Zealand

Leave A Comment